China Rapid Finance is the largest and fastest growing consumer lending marketplace in China in terms of number of loans facilitated.

According to the People’s Bank of China, or the PBOC, as of the end of 2014, there were approximately 500 million individuals with quality employment records but no credit history. We view these individuals, who also regularly use mobile devices, as our target market and refer to them as EMMAs (Emerging Middle-class,

Mobile Active consumers). We generate recurring fee revenue from borrowers and investors, including transaction and service fees for loans facilitated on our marketplace.

To find and attract EMMAs, China Rapid Finance has developed China’s definitive proprietary credit assessment and pre-screening technology featuring its: Predictive Selection Technology and Automated Decisioning Technology.

- Payment data provided by its institutional and payment system partners

- Credit data developed over more than 5 years facilitating loans to Chinese consumers

- Social data assembled through partnerships with multiple internet companies. We are also building multiple channels with online travel agencies, online group-buy and shopping platforms, online gaming companies, online e-commerce platforms and payment service providers to enable us to reach more potential qualified EMMA borrowers.

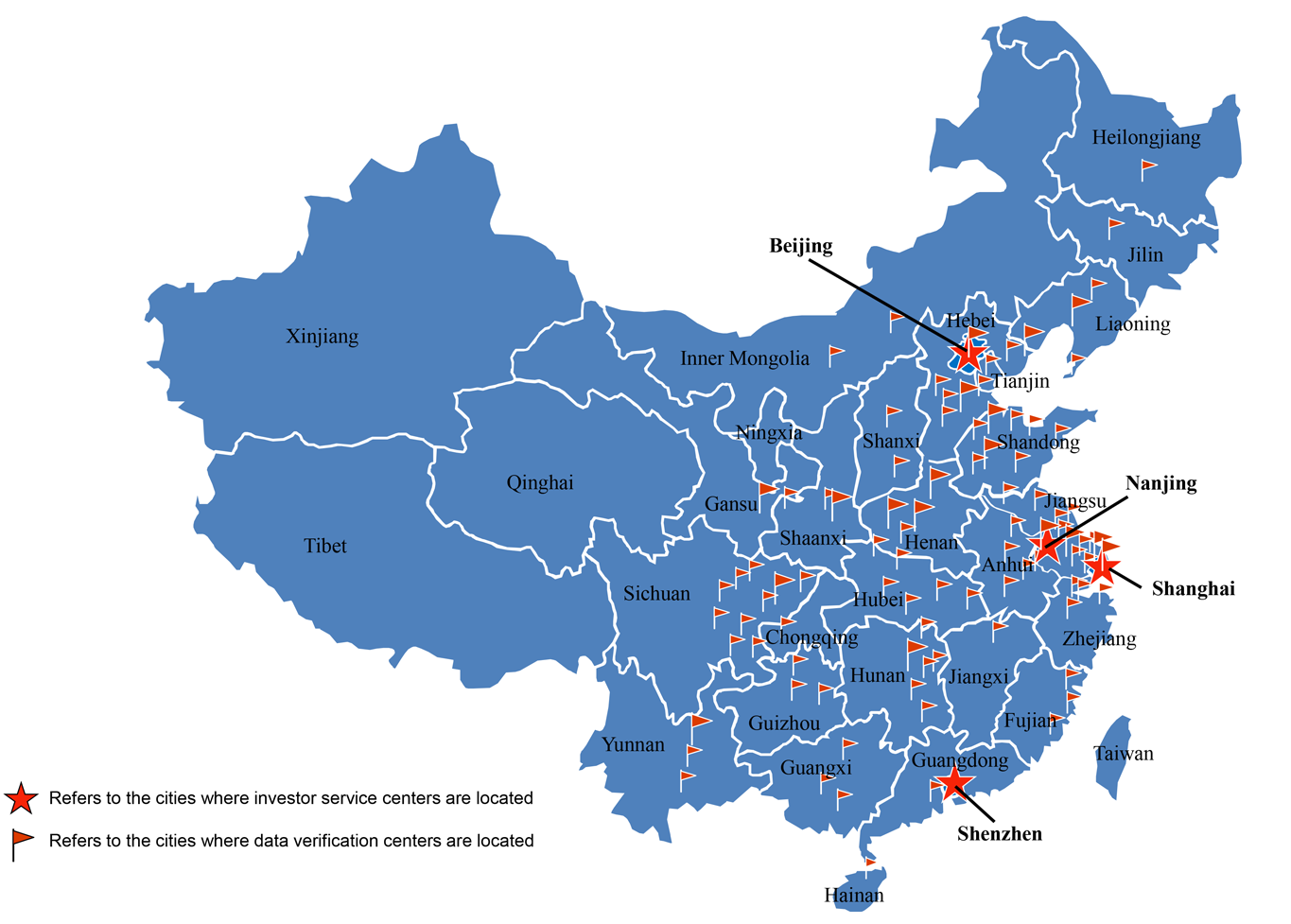

- Anti-fraud and collection information collected through an extensive network of offline data verification centers (90+ cities)